Weekend Developments – OPEC, Oil, PBOC RRR Cuts, EU Response to US Auto Tariff Threat

Crude oil prices started off the new week with declines after Friday’s impressive performance saw it rally the most in a single day (+5.32%) since November 2016. There, the commodity rose as the real production increase agreed in the OPEC+ meeting amounted to a real gain of less than expected (+600k bpd versus 1 million).

However, over the weekend, comments from Saudi Energy Minister Khalid Al-Falih downplayed those pessimistic expectations. He said that the total OPEC+ oil hike will be closer to 1 million barrels per day versus +600k. Not only that, but he added that they will do ‘whatever is necessary’ to keep the market in balance. Russian Energy Minister Alexander Novak then reiterated Al-Falih’s view.

Meanwhile, the People’s Bank of China cut the reserve ratio for qualified banks by 0.5 percentage points. Cutting the RRR is essentially another form of monetary policy that can stimulate an economy. This frees up more cash in banks for the use of lending and can boost liquidity. According to the PBOC, these actions are to release about 500b Yuan for debt-to-equity projects.

In a follow-up to Friday’s 20 percent auto tariff threat from US President Donald Trump, EU commissioner Jyrki Katainen said that that bloc would again have ‘no choice’ but to react. Escalating trade war tensions can have consequential impacts on sentiment. However, so far the opening to this week’s session was rather quiet. The anti-risk Japanese Yen was slightly higher while the sentiment-linked Australian Dollar was lower.

A Look Ahead – FX, Stocks Eye Risk Trends. CAD May Fall

A lack of key economic event risk during Monday’s Asian trading session will probably have markets eyeing risk trends. Rising trade tensions between the EU and US, in addition to China and Canada, could send some benchmark indexes lower. Such an outcome can boost the Yen at the expense of high-yielding currencies such as the New Zealand Dollar.

The Canadian Dollar, hurt by a worse-than-expected local CPI report, managed to pare its losses. This may have been due to the remarkable rise in crude oil prices. For Canada, since the commodity is a key source of revenue, price changes can have knock-on effects on growth and thus inflation expectations. If oil prices continue declining on the OPEC weekend news, then we may see a pullback in the Canadian Dollar.

DailyFX Economic Calendar: Asia Pacific (all times in GMT)

DailyFX Webinar Calendar – CLICK HERE to register (all times in GMT)

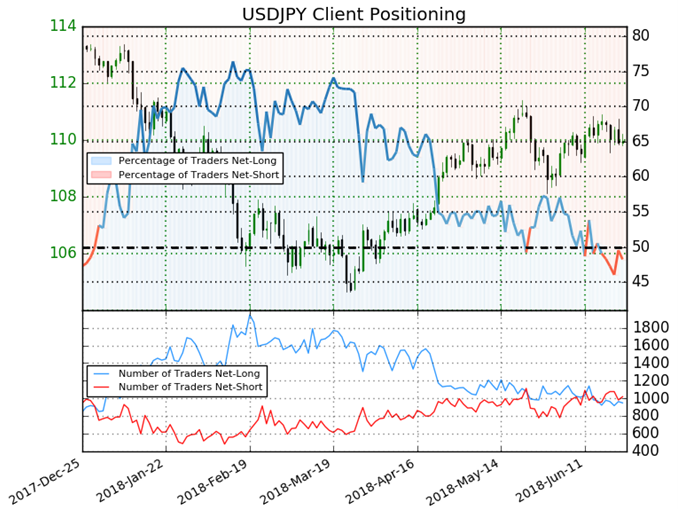

IG Client Sentiment Index Chart of the Day: USD/JPY

CLICK HERE to learn more about the IG Client Sentiment Index

Retail trader data shows 48.2% of USD/JPY traders are net-long with the ratio of traders short to long at 1.07 to 1. The number of traders net-long is 2.8% lower than yesterday and 7.5% lower from last week, while the number of traders net-short is 2.0% higher than yesterday and 0.7% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise. Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bullish contrarian trading bias.

Five Things Traders are Reading:

- Fundamentals Support a USDJPY View but Hopelessly Complicate EURUSD by John Kicklighter, Chief Currency Strategist

- EUR/USD Weekly Technical Outlook: Euro Bounce Set Up to Fail? by Paul Robinson, Market Analyst

- Australian Dollar’s 360 Degree Hammering Likely To Continueby David Cottle, Analyst

- New Zealand Dollar May Fall on US Data and Trade Wars. Not RBNZ by Daniel Dubrovsky, Junior Analyst

- USD/JPY Breaks the June Bullish Trend Despite Continued Inflation Lagby James Stanley, Currency Strategist

— Written by Daniel Dubrovsky, Junior Currency Analyst for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter